In keeping with the continuous nature of cryptocurrency and digital asset trading, the RULEMATCH trading venue operates seven days per week, 365 days per year over a trading day of 23.5 hours.

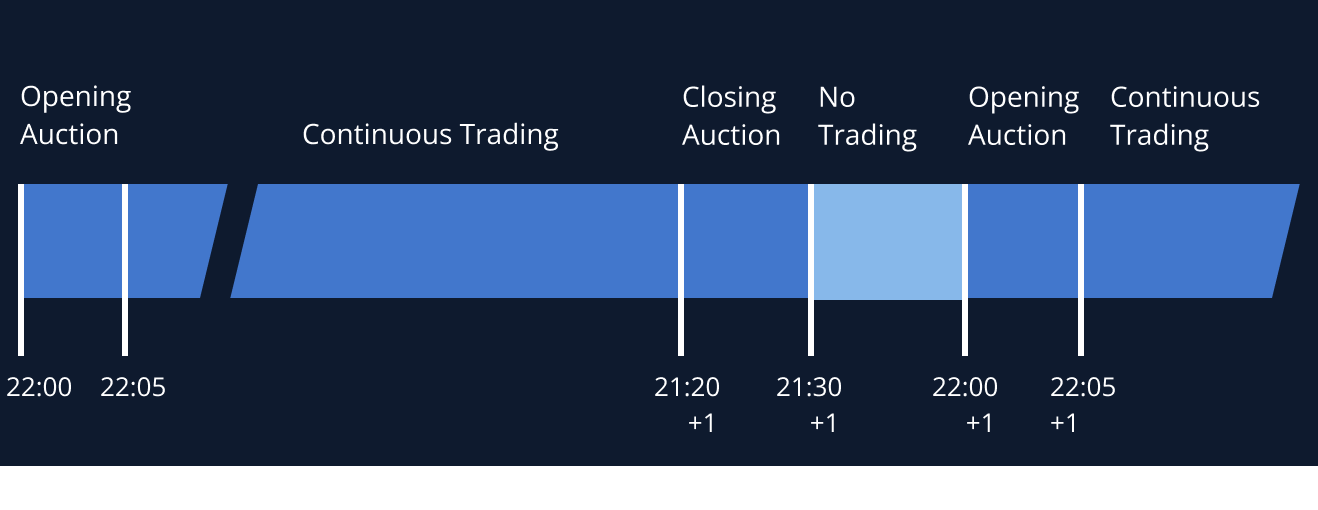

The trading day at RULEMATCH lasts from 22:00 to 21:30 (+1) UTC and is divided into three separate trading sessions:

Opening auction: 22:00 – 22:05 UTC

Continuous trading: 22:05 – 21:20 (+1) UTC

Closing auction: 21:20 – 21:30 UTC

Each trading session is dictated by specific rules with respect to order entry, which are highlighted in the Order Types section.

A trading day is followed by the close of trading that lasts from 21:30 to 22:00 UTC. During the close of trading no orders/quotes can be placed.

Trading days from Monday to Thursday are each represented by one trading cycle. From Friday to Sunday, the trading days are grouped into one, single trading cycle (“extended trading cycle”).

Continuous trading allows orders and quotes to be immediately matched according to the rulebook of RULEMATCH.

Incoming orders are, from a trading perspective, always considered as aggressive and compared to the passive orders in the book for potential matching.

Opening and closing auctions consist of an interest collection phase, followed by an uncross, which is used to execute possible matches. During the interest collection phase, orders and quotes are accepted and allowed to cross without any matching. The uncross is performed in the transition to the next session, with the equilibrium price of the auction used as the matching price. All orders are considered passive during an auction, irrespective of their attributes.

The equilibrium price is calculated and disseminated by the matching engine throughout the duration of the auction, assuming there are crossed orders in the central limit order book.

The prices used in the selection of equilibrium price are all valid price ticks between and including the highest and lowest limit orders crossing and locking the market, extended with one tick up from the highest and one tick down from the lower limit price. With these eligible prices, the equilibrium price is calculated using Nasdaq’s proprietary algorithm that seeks to maximize the executable quantity while minimizing any potential surplus.