Participants trade on the venue using collateral pledged to cover the open market, as well as clearing and settlement risk. RULEMATCH allows for multi-collateral portfolios valued in USD – which is also the currency used for margining purposes.

Margin on RULEMATCH is comprised of an Initial Margin (IM) component (reflecting the potential market risk), and a Variation Margin (VM) component (reflecting the current Mark-to-Market valuation).

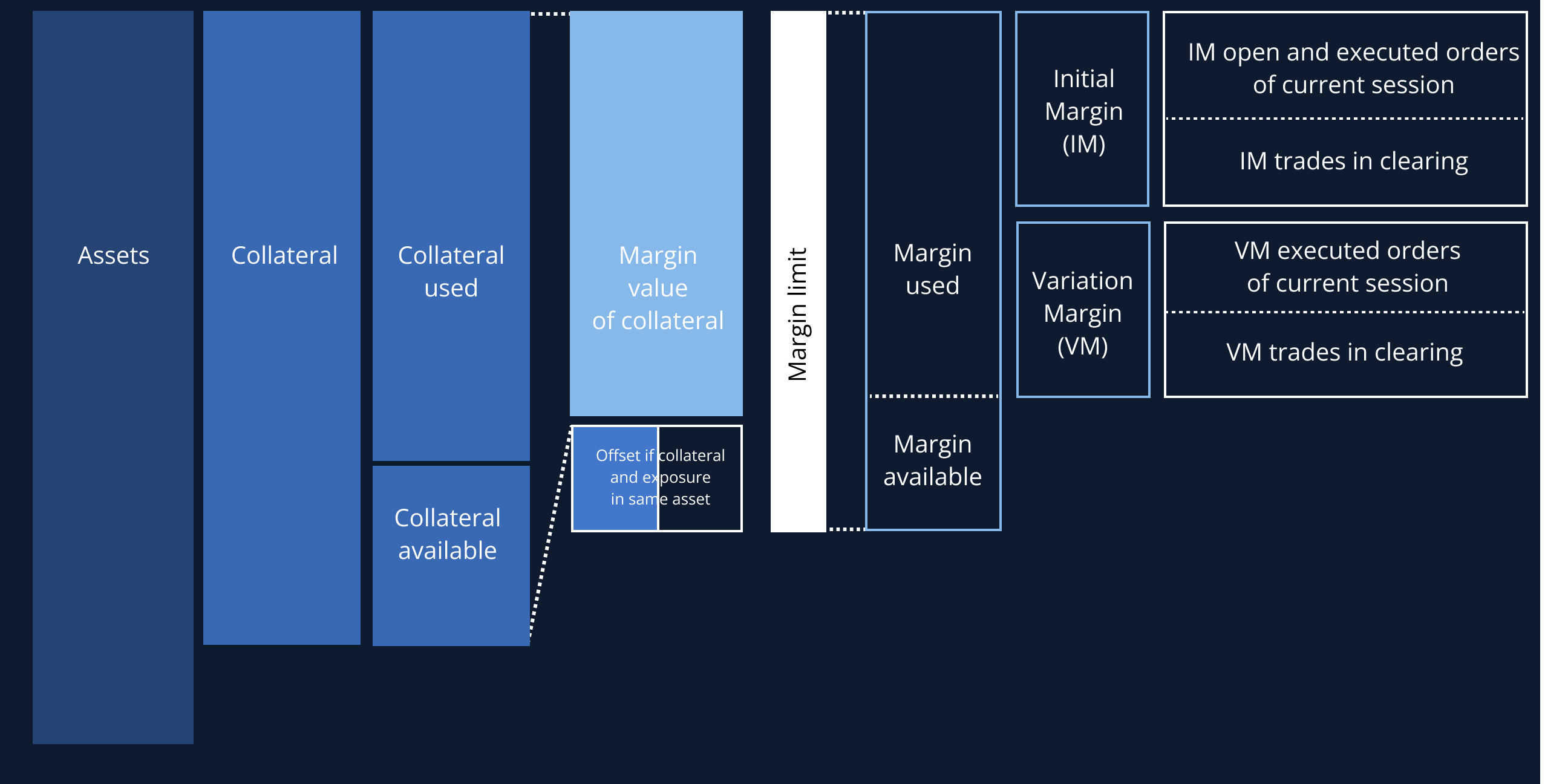

The collateral and margining landscape of RULEMATCH is depicted below. This graph is further used as a reference in the individual descriptions of each component.

The collateral and margining landscape for RULEMATCH participants.

Assets: The USD-denominated value of all assets being held in the account.

Collateral: The USD-denominated value of all assets assigned as collateral in the account. Only assets that are not submitted as obligations of a clearing cycle or are not currently quarantined are free to be used as collateral.

Collateral used/available: The ratio of collateral used over the full collateral is always equal to the ratio of margin used over the margin limit. Hence, if an account is currently utilizing 60% of the margin limit, collateral used will also be equal to 60% of the collateral. Collateral available is equal to the remaining amount (e.g. 40%), and serves as a rough indication of the unutilized liquidity that could be withdrawn from the reserved collateral, without causing a breach of the margin limit.

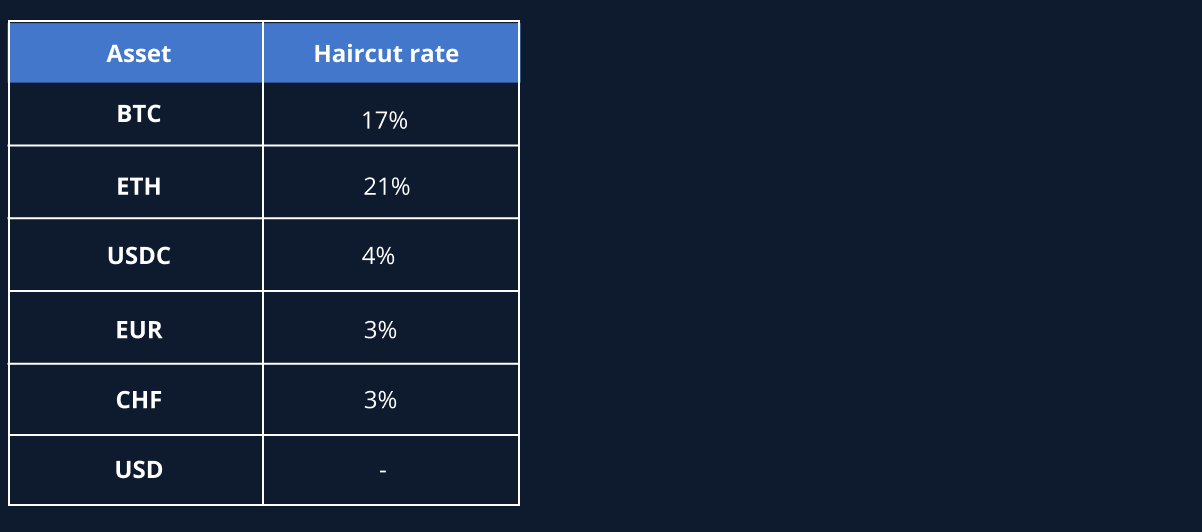

Margin value of collateral: The USD-denominated value of the collateral, after the haircut rates have been applied per asset. The table below indicates the current haircut rates for each tradeable asset.

Matched collateral benefit: In the case of both collateral and trading/clearing exposure being on the same asset, the volatility of that asset no longer contributes to additional risk. As a result, the haircut rate is reversed, up to the amount of the exposure itself, and not the full amount of the collateral.

Margin limit: The sum of “Margin value of collateral” and “Offset if collateral and exposure in same asset”. This amount ultimately defines the maximum amount of trading and clearing exposure the participant’s account can undertake.

RULEMATCH allows all tradeable currencies of the venue to be used as collateral, plus EUR and CHF. The collateral portfolio is valued in USD terms, considering the volatility of collateral assets by applying an individual haircut on each asset’s USD valuation.

The valuation of the collateral ultimately leads to the margin limit, which defines the maximum amount of trading and clearing exposure the Participant’s account can undertake.

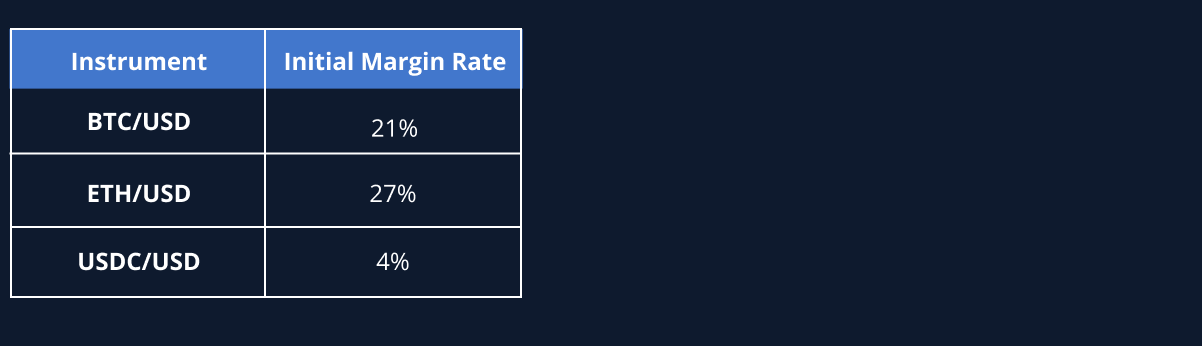

Initial margin: IM represents the open market risk of the orders and trades placed on the participant’s account. It is calculated for both open and executed orders of the current trading session, as well as trades executed on the previous session that are now open for clearing and settlement. The sum of the two leads to the full initial margin.

The IM for open and executed orders of the current trading session is based on the open exposure per instrument, which is calculated as follows.

Open exposure per instrument = Max (Total Net Buy, Total Net Sell), where:

Total Net Buy = Traded Bought – Traded Sold + Open Buy Orders

Total Net Sell = Traded Sold – Traded Bought + Open Sell Orders

By choosing the maximum of the two metrics, the open exposure indicates the net position of the account with the highest market risk for each instrument, which is then converted into USD and multiplied by the IM rate of the instrument. The value for each instrument is then summed.

Trades of the previous session, currently open for clearing and settlement are also netted for each individual instrument, and the net open position is valued in USD and multiplied by the IM rate of the instrument.

The table below indicates the current IM rates per instrument.

Variation margin: VM represents the current profit and loss position stemming from the trading activities on the participant’s account. It is calculated for both the current as well as the previous session’s trading activities that are currently open for clearing. The sum of the two (for all applicable instruments) leads to the full variation margin.

Margin used: The full margin used is calculated as the sum of IM and VM. It is important to note that IM is always increasing the margin used for the account, while VM could either decrease or increase it, depending on whether the account is at a mark-to-market profit or loss.

Margin available: The difference between the margin limit and margin used leads to the margin available on the account. This metric is split between the tradeable instruments of the venue, based on a percentage allocation defined by the participant on each account (e.g. 60% BTC/USD – 40% ETH/USD). The participant has the ability to configure this allocation at any point through the UI of RULEMATCH. Once the available margin for an instrument has been breached, the account is no longer able to enter orders on this instrument. The participant would have to either bring more collateral to the account, allocate more available margin on the instrument, or reduce the exposure by e.g. removing open orders or executing a risk-reducing trade, to re-enable order entry. It is important to note that maximum order size is also limited by the available margin, in order to restrict participants from entering an order that would lead to a breach of the margin limit.